Contact Us : 800.874.5346 International: +1 352.375.0772

Very. The overall CPA Exam pass rates hover slightly below 50%. This makes passing the CPA Exam a difficult, but achievable, goal. You’ll need to study wisely, set a strategy for managing your time, and call on your support network, but with the right plan and good study materials, you will conquer it.

Passing the CPA Exam is an accomplishment to proud of. We’ll show you how.

The AICPA does not limit the number of times you may take the CPA Exam. With a pass rate of ~50%, steep examination requirements, and regularly updating materials, many candidates will find themselves taking one or more sections multiple times on their path to the CPA certification.

The CPA Exam is so difficult because:

It covers a wide variety of topics at different skill levels.

It tests those topics using multiple question types, including some that simulate real-world tasks CPAs are expected to perform.

You have a limited amount of time (30 months from when you pass your first section) to pass four sections.

Each section is timed.

The CPA exam consists of three required core section exams, and three discipline section exams, where you will have to choose one discipline to study and pass.

The hardest topic on the CPA Exam for you depends on your accounting background. While many candidates find the FAR section to be the most difficult, you may consider AUD more difficult if you’ve never completed an audit, or REG with its focus on tax law to be the most challenging, for example.

Ultimately, it isn’t any one topic or section that makes the CPA Exam difficult—it’s the sheer scope of the exam in its entirety. Within it’s content areas are almost 600 representative tasks. Each task represents a key knowledge or skill required of CPAs, and these tasks are judged at different difficulties or skill levels.

THE GLEIM SOLUTION

Gleim CPA Review takes all the guess work out of the representative tasks.

Each question and simulation in our test bank has been crafted to test different tasks at their respective knowledge levels. And our SmartAdapt™ technology will monitor your progress on each of these content areas and ensure you see the materials you need to see to be prepared on exam day.

| AUD Content | ||

|---|---|---|

| AREA | PERCENTAGE | |

| Ethics, Professional Responsibilities, and General Principles | 15-25% | |

| Assessing Risk and Developing a Planned Response | 25-35% | |

| Performing Further Procedures and Obtaining Evidence | 30-40% | |

| Forming Conclusions and Reporting | 10-20% | |

| REG Content | ||

|---|---|---|

| AREA | PERCENTAGE | |

| Ethics, Professional Responsibilities and Federal Tax Procedures | 10-20% | |

| Business Law | 15-25% | |

| Federal Taxation of Property Transactions | 5-15% | |

| Federal Taxation of Individuals | 22-32% | |

| Federal Taxation of Entities | 23-33% | |

| FAR Content | ||

|---|---|---|

| AREA | PERCENTAGE | |

| Financial Reporting | 25-35% | |

| Select Blanace Sheet Accounts | 30-40% | |

| Select Transactions | 20-30% | |

| BAR Content | ||

|---|---|---|

| AREA | PERCENTAGE | |

| Business Analysis | 40-50% | |

| Technical Accounting and Reporting | 25-35% | |

| State and Local Governments | 30-40% | |

| ISC Content | ||

|---|---|---|

| AREA | PERCENTAGE | |

| Information Systems and Data Management | 35-45% | |

| Security, Confidentiality, and Privacy | 35-45% | |

| Considerations for System and Organization Controls (SOC) Engagements | 30-40% | |

| TCP Content | ||

|---|---|---|

| AREA | PERCENTAGE | |

| Tax Compliance and Planning for Individuals and Personal Financial Planning | 30-40% | |

| Entity Tax Compliance | 30-40% | |

| Entity Tax Planning | 10-20% | |

| Property Transactions (Disposition of Assets) | 10-20% | |

While memorization may have been enough for passing CPA Exam versions in the past, the modern CPA Exam expects more from candidates. The current exam version will compel you to reach a greater comprehension of accounting topics by featuring questions that assess you for higher levels of knowledge and skill.

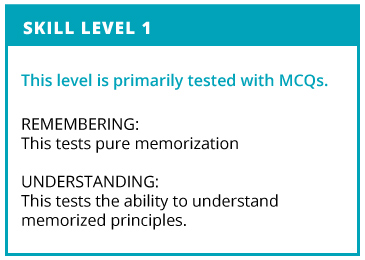

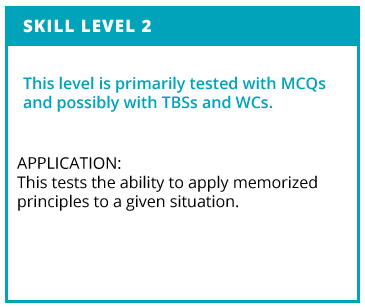

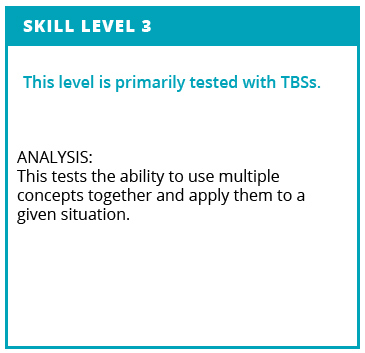

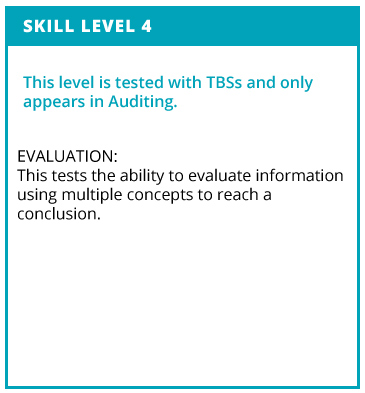

The CPA Exam Blueprint, an outline of the topics that can appear on the CPA Exam, includes representative tasks that the AICPA has determined are critical for newly licensed CPAs to understand. The CPA Exam incorporates these tasks into its questions, and the AICPA has assigned one of the following four skill levels to each of the tasks.

Remembering and Understanding requires the lowest amount of skill, while Evaluation requires the highest amount.

To reach the Analysis and Evaluation levels, you must answer the “so what” questions: Explain why something is important or not important. CPA Exam questions that ask you to reconcile, conclude, or evaluate scenarios address the higher skill levels.

Only AUD will test you at the Evaluation level, but all of the exam sections will test you up to the Analysis level

Each section of the CPA Exam is divided into 5 testlets. Two consist of only Multiple-Choice Questions, and three contain just Task-Based Simulations.

| Section | Remembering and Understanding | Application | Analysis | Evaluation |

|---|---|---|---|---|

| AUD | 25%-35% | 30%-40% | 20%-30% | 5%-15% |

| FAR | 10%-20% | 50%-60% | 25%-35% | – |

| REG | 25%-35% | 35%-45% | 25%-35% | – |

| BAR | 10%-20% | 45%-55% | 30%-40% | – |

| ISC | 55%–65% | 20%-30% | 10%-20% | – |

| TCP | 5%-15% | 55%-65% | 25%-35% | – |

These CPA Exam sample questions demonstrate some of the range in difficulty that these skill levels test.

The AICPA uses different types of questions to test its material. To ensure your success on the CPA Exam, you’ll need to have experience with each type of question prior to sitting for the exam.

On the CPA Exam, Multiple-Choice Questions contain a question stem and four answer choices. Three of the answer choices are known as distractors. These are tricky because they are based on common errors or misconceptions. The correct answer will be the best response to the question stem.

Task-Based Simulations are designed to mimic common tasks that accountants face. These include preparing journal entries, correcting memos or emails, researching regulations and laws, and collecting data from different sources.

Many TBSs will require you to use different exhibits provided in the simulation to collect the data needed to complete a given task.

THE GLEIM SOLUTION

Gleim CPA Review ensures you will face no surprises on exam day. With more than 10,000 Multiple-Choice Questions modeled after actual AICPA questions and with over 1,300 simulations just like those you’ll see on the exam, you can be certain that you’ll be well prepared for even the most difficult questions on the CPA Exam.

Every CPA Exam section has Multiple-Choice Questions and Task-Based Simulations. Below is the breakdown of the question types you’ll see on each CPA Exam section.

| Question Types on the CPA Exam | ||||||

|---|---|---|---|---|---|---|

| Section | AUD | FAR | REG | BAR | ISC | TCP |

| Testlet 1 | 39 MCQs | 25 MCQs | 36 MCQs | 25 MCQs | 41 MCQs | 34 MCQs |

| Testlet 2 | 39 MCQs | 25 MCQs | 36 MCQs | 25 MCQs | 41 MCQs | 34 MCQs |

| Testlet 3 | 2 TBSs | 2 TBSs | 2 TBSs | 2 TBSs | 1 TBSs | 2 TBSs |

| Testlet 4 | 3 TBSs | 3 TBSs | 3 TBSs | 3 TBSs | 3 TBSs | 3 TBSs |

| Testlet 5 | 2 TBSs | 2 WCs | 3 TBSs | 2 TBSs | 2 TBSs | 2 TBSs |

| Total MCQs | 78 | 50 | 72 | 50 | 82 | 68 |

| Total TBSs | 7 | 7 | 8 | 7 | 6 | 7 |

The Task-Based Simulations are the most difficult part of the exam for most candidates. These questions require candidates to interpret information from multiple sources and complete multiple tasks using that information. Additionally, the fact that they come after both MCQ testlets means you’re already well into your exam time and mental fatigue may have begun to set in.

The CPA Exam has two time limits, and both affect the difficulty of the exam. The first time limit you will face is the four-hour duration of each section’s exam. After you pass your first section, you’ll encounter the second time limit: the 30 months for which your passing score remains valid.

When you sit down for the CPA Exam, you’ll see a small countdown clock in the top-left corner of your screen. It will display in hours:minutes and will begin counting down as soon as you are through the five-minute introductory screens.

This countdown will be one of your greatest enemies during the exam. You have to really manage your time well if you want to finish within the allotted time and pass the exam.

Each exam section has a different number of Multiple-Choice Questions and Task-Based Simulations, so you will need a winning time management strategy in order to pass each section on your first attempt!

Your task is to answer each of these questions to the best of your ability. But having a time limit means you’ll need to prioritize answering every question over scrutinizing each question individually.

To make matters worse, during the CPA Exam, you will not be able to return to testlets once you have completed them. It is vital to plan your time in each testlet because any extra time you have at the end of the exam is wasted.

THE GLEIM SOLUTION

Because the CPA Exam’s time limit is not divided between testlets for you, it is important to plan your test time before you sit for the exam.

The Gleim Time Management System sets time goals for each testlet of the CPA Exam. By following our time allocation recommendations, you can ensure you have enough time for each question in every testlet.

You can learn more in our free CPA Exam Guide.

Once you have passed your first section of the CPA Exam, a new timer begins counting down. You have 30 months to pass your remaining three sections of the CPA Exam; if you do not pass them all, you’ll lose credit for the first section you passed.

This adds additional stress to every stage of your exam process. Managing this stress, creating a study plan, and adjusting your plans for setbacks is part of passing the CPA Exam.

Time-management and project management are key skills for accountants to possess. By including multiple time limits on the CPA Exam, the AICPA tests your ability to manage time and maintain accuracy and focus.

We have tips on how to schedule your exam sections to make sure you beat the 30-month time limit.

THE GLEIM SOLUTION

The CPA Exam’s 30-month time limit makes it critical to plan ahead.

With Gleim’s Study Planner and Personal Counselors, you’ll have the tools you need to plan your exam schedule. An ideal schedule will be flexible enough for emergencies and additional hurdles—but firm enough for goal setting.

Gleim’s Personal Counselors have helped candidates pass over a million CPA Exams, so you can rely on their expertise.

Within 30 months of passing your first CPA Exam section, you must have passed four sections or you will lose credit for that first section. Then, you must pass any remaining sections and any section(s) you lost credit for within 30 months of the oldest section you still have credit for.

The CPA Exam is made up of four sections and each section includes four hours of testing time and one hour of time for administration and security. The exam is offered year-round, and scores only remain valid for 30 months.

In other words, the CPA Exam is a long exam, and this time investment makes every aspect of it that much harder.

The time invested into the CPA Exam will come in two main chunks: studying for the exam and taking the exam.

Studying for the CPA Exam is a time-consuming process. Every candidate’s experience will be different. We’ve seen candidates pass with as little as 80 hours of study time per section, and we’ve seen others need 180. The study time you need can be influenced by factors such as how familiar you are with the material, how long it’s been since you earned your degree, and how long ago you last studied for a serious exam. Ultimately, planning your study schedule is just another aspect of the difficulty of the CPA Exam. If you invest too little time, you risk poorly covering key topics. Invest too much, and you could begin forgetting topics covered near the beginning of your studies.

The Gleim Premium CPA Review Course is a complete course to help you not only plan out your studies but overcome the challenges of studying for such a difficult exam. Our SmartAdapt™ system keeps track of your progress and presents previously mastered questions to ensure you don’t forget a single topic!

The average CPA candidate may need 6-12 months to pass the entire CPA Exam. This could vary depending on:

You will likely spend more time taking the exam than you imagined, once you consider the additional time spent traveling, scheduling, and signing in.

According to Prometric’s Candidate Bulletin, you will need at arrive to the testing site 30 minutes before your appointment time. This time is spent verifying your identity and reviewing the testing center policies. If you do not arrive at least 30 minutes prior to your scheduled time, you may forfeit your appointment and will receive no refund!

In addition, while the CPA Exam is four hours, your appointment will be scheduled for four and a half hours to include time for the survey and optional break. Do not confuse this time with the 30 minutes required by Prometric. With each exam taking five hours, the CPA Exam will require a minimum of 20 hours of examination time!

Scheduling concerns for international candidates

If you’re an international candidate, the travel time can be especially difficult if the CPA Exam is not offered in your home country.

It is not unheard of for international candidates to schedule all of their exams within a week of each other in order to minimize what may otherwise be one of the largest hurdles between you and the CPA certification.

| CPA Exam Time Per Section total 5 hours |

|||||

|---|---|---|---|---|---|

| Prometric Sign-in | CPA Exam Introductory Screens | Testlets 1,2, & 3 | Break | Testlets 4 & 5 | CPA Survey |

| 30 minutes | 10 minutes (Two at 5 minutes each) | 144 minutes | 15 minutes (optional*) | 96 minutes | 10 minutes |

*Note: Although this 15-minute break is optional, we highly recommend taking this break so you can remain focused for the remaining test time. Bring a small snack to keep in your locker, or use this time to stretch and refocus.

Between this and any travel or accommodation time that may be required based on the testing center of your choice, it is clear that time plays a significant role in test-day stress.

We repeat: Time-management skills are vital to overcoming the CPA Exam!

The CPA Exam is a time-consuming exam, so it is important to make sure it only eats as much of your time as it absolutely has to. You will spend approximately 30 times as long studying for the exam as you will actually spend taking it, so it can be tempting to shave that study time down to sit for the exam faster. But cutting too many corners can cost you—studying for an exam section a second time will more than erase any time you might have saved.

See the list below for some tips on how to and how NOT to save time on the CPA Exam.

CPA Exam Time-Saving Tips

Spend most of your time on topics you’re struggling with

Set aside time specifically to study—and set study objectives

Practice all of the question types

Use the CPA Blueprint as a guide on study topics

Take the Exam when you are consistently scoring 80% on your practice tests

Completely ignore topics you’re comfortable with

Plan to study all day, every day

Memorize the individual questions

Ignore topics you don’t think will be tested

Wait until you are scoring 100% on all of your practice tests

As you can see from our tips, the key is to study smart. Under preparing will result in poor performance, and failure means more time spent registering, traveling, and testing. Over preparing will consume your time and can cause information to become dated as the CPA Exam changes.

Our biggest suggestion is this: Find a CPA review provider that will help you with CPA Exam prep. The time you would otherwise spend deciphering the exam blueprints and figuring out what to study would be better used studying your materials so you can pass the CPA Exam.

There’s no doubt the CPA Exam is hard, but this difficulty is by design. There are two main factors contributing to the CPA Exam’s difficulty:

Understanding why this exam is so difficult can help motivate you to get through it.

The CPA Exam has two primary purposes: to provide reasonable assurance of a candidate’s skills and to retain the value of the CPA certification.

Providing assurance of a candidate’s skills will always be the most important role of the CPA Exam, and accomplishing that task is the main reason the CPA Exam is hard.

This requires the CPA Exam to constantly adjust to new laws, regulations, and industry standards and continually push the difficulty of the exam to meet the expectations of companies and lawmakers.

Every time the AICPA updates the CPA Exam, it has to ensure the content:

In addition, the CPA Exam’s difficulty ensures that it continues to be the gold-standard for accountants. The exam’s difficulty is one of the reasons why the certification is sought after by so many aspiring accountants.

It’s also why CPAs make 10-15% higher salaries than non-certified accountants.

The modern economy has changed the expectations and responsibilities of accountants. The ability to interpret and apply laws and regulations has become an expected and crucial part of the accounting profession. As a result, the CPA Exam must continually adapt to include the new and higher standards demanded of accountants.

The AICPA also regularly surveys leaders in the accounting industry to keep pace with the evolving needs of accounting firms serving their clients. These surveys, called Practice Analysis, provide insight on the expectations of newly-licensed CPAs. These changes ensure that the CPA certification remains relevant to all accounting career paths, regardless of how the accounting field changes.

When the AICPA was formed in 1957, the CPA Exam had already existed for 40 years.

The CPA Exam was originally designed in 1917 as a test for membership to the Institute of Public Accountants (the organization that would eventually become the AICPA). Prior to this test, each state would issue its own exam, a practice that many states continued until 1952 when the CPA Exam became the universal standard.

The exam has changed many times over the years. Originally, the 19.5-hour-long exam was administered in five sittings over two and a half days, only twice per year. It wasn’t until the paper-and-pencil exam was discontinued in 2004 that the exam began to look like it does today.

From the very beginning the CPA Exam needed to be hard because it served as the standard for what an accountant needed to know. In those days, passing the CPA Exam might have been the only signifier accountants had to prove their mastery of accountancy!

Back in 2006, the CPA Exam pass rates for all four sections showed little variation. However, they began to diverge in 2011 due to the massive change the CPA Exam went through that year, the largest changes since the exam became computerized in 2004.

You can read more information on recent pass rates on our CPA Exam Pass Rates Guide page.

Understanding the difficulty lets you plan ways to overcome the hurdles and gives you perspective on the skills that the AICPA considers most valuable in the modern CPA candidate: excellent time- and project-management skills, a thorough understanding of accounting, and the ability to communicate and use knowledge and experience.

Gleim is here to help. Read more about the features and tools that Gleim offers at our CPA Exam Resource Center and start your journey to passing the CPA Exam today!